Craft

Four works of art that show attention to craft, from peculiar artists, with particular takes. All recommended if that sounds interesting.

Four works of art that show attention to craft, from peculiar artists, with particular takes. All recommended if that sounds interesting.

I started to get dizzy in January 2023. It began with ringing in my ears after attending a loud concert and gradually worsened. Some days, it was debilitating, almost like being on a spinning ride. Other days, it felt more like being on a constantly rocking boat. They called it vertigo, and when doctors use that term, they take it seriously and subject you to numerous tests to determine the cause. In my case, they were unable to pinpoint a definitive reason, and after about 45 days, the symptoms lessened and eventually disappeared over the next few months. During these investigations, they also discovered high-frequency hearing loss in my auditory range - completely unrelated to the vertigo! - but most likely caused by years of exposure to loud live music.

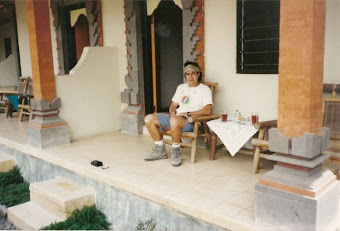

This reminded me of my friend Keith who was one of my concert-going friends a long time ago. Keith and I backpacked around Asia after we graduated from school. I’d like to think we were a good duo as Keith pushed me towards adventure (“don’t worry it’s safe if we give them our passports to rent these motorcycles”) and I got us to Bangkok and back from Singapore many months later. One time he hiked to the top of Mt Batur on Bali at sunrise while I stayed behind, too sick with food poisoning to join him. When he returned he took a photo of me recovering with one of the few disposable cameras we brought to document our trip. Back then, there were no mobile phones to capture memories in an instant. Even though we talked about our travels often for years afterwards, I never really told Keith how meaningful the whole thing was. We have those few photos, though.

This got me thinking: the area codes linked to our phone numbers once indicated our current location, but now they represent our place of origin.

That change in perspective gave me an idea: in a world of abundance, the real question is not what we can do but rather what we should. What if the aperture of what was available was then, and instead, narrowed down and limited? Imagine a service that offered only one item within your desired category. Then I poked around and noticed that others were also thinking about this same thing.

Fair Warning is an art service that auctions only one piece of art every other week or so.

1001 Albums wants you to listen to all the great albums of all time but only presents one a day to you. Dudel Draw is an app that gives you one new shape every day to draw on. One Thing is a newsletter about one interesting thing, each time.

What if there was a movie service that offered only one film per week, exclusively on Wednesday nights? And once the movie was gone, it was gone for good. The catch? You wouldn't even know what the movie was until two days before it played. Is this interesting or just a gimmick?

The concept of narrowing focus made me think about this thing my friend R and I do. We send cold emails to interesting people we want to meet, obsessing over who we choose and what we write. Most of the time, these emails go unanswered, but I’ve come to realize that's not the point. It's not about getting a response; it’s about the idea of doing the act itself, challenging yourself, and taking a (small) personal risk. Maybe it's more about the idea or memory of doing it than actually doing it.

These emails reminded me of something Sarah Manguso wrote: “The first beautiful songs you hear tend to stay beautiful because better than beauty, which is everywhere, is the memory of first discovering beauty.”

I remembered something else that has beauty: the Jewish custom of saying “may their memory be a blessing” when someone dies. They may no longer be with us, yet their memory remains a gift and a blessing.

All these thoughts made my mind drift to a few weeks ago when I found myself in a tiny basement bar in the West Village late into the night on a random weeknight and a jazz trio was playing mid tempo songs and people were drinking martinis and talking loudly and strangers were dancing and it felt like the center of the universe. Ever get that feeling?

Right before the holidays we made a film.

We wanted to do something special at USV's year-end event to celebrate a milestone. We asked friends of the firm to record videos marking the event. These would be simply strung together to watch.

When the videos started arriving five days before the event, we realized we were about to sit through something like a wedding video on an oversized TV at a family gathering.

Help: we needed a reset, immediately.

A movie, like a tapestry, wanted to be woven from these raw materials. Yet, we didn't know how to begin the process of filmmaking. Let's go. The five-day sprint that ensued was like a last-ditch effort to catch a moving train.

Step one: cobble together a patchwork of cloud tools to upload and store the videos. Step two: learn, quickly, how to edit. Step two was more daunting. In a moment of something between howling desperation and creative inspiration, we recalled the class of new intelligent creative tools (yes, powered by AI) that provide text-to-edit and other "magic" edit functionality (RunwayML, Descript). We dove in eyes closed head first full hearts.

No tutorials, there wasn’t time. Learn by doing. The tools were the key, the elixir that enabled the blank canvas to look less intimidating; to turn thoughts and ideas into output and expressions, almost instantaneously.

We uploaded. Cut and pasted video. Inserted fade-ins and fade-outs. Added music and audio for format diversity. Spliced in movie clips (Casablanca, History of the World Part I, Swingers) to break up the talking heads. Found a perfect ending song; maybe it wasn't. Yes it was.

From an hour of raw material, we ended up with a five-minute short “film.”

It was grueling, demanding and degrading. Also invigorating. Above all else: all-consuming. Waking up at 3 am to jot down ideas. Executing those ideas at 6 am. Changing your mind at 10 am and removing them. Reverting back to the idea the next day at 6 am. And so on, each day, for those five days. Time evaporated like water on a stovetop. On three separate occasions we declared pencils down. Finished. But, more adding and subtracting. Just one more edit.

Hours before showtime, the moment of truth arrived. Time had run out, the event was starting, and there was no choice but to be done, like the landing of a jet (or the crashing of a jalopy).

On the final day, each time I viewed the film I flipped between loving it . . . and hating it. Extremes: the love was intense; the embarrassment was debilitating, like sharp icicles in my chest. Was this an act of creativity or a foolish mission by an amateur poseur? “Is this good?” we kept asking ourselves.

I reached out to a filmmaker and texted:

“When you finish a project, do you ever look at it and think, ‘this is the worst thing ever created?’ ”

“Welcome to my torment” he replied.

The thing is, it's clear that this wasn't about making a good film. As I look back on it - though I can't bear to watch it again - this was about a blank page. Kerouac once wrote “The page is long, blank, and full of truth. When I am through with it, it shall probably be long, full, and empty with words.”

The words - or paint, or sound, or moving images - are only a conduit for meaning, but may never be the meaning itself. The question thus becomes: how fast can you get to the conduit, to fill the blank canvas?

Technology facilitates this. Accelerates too. Reduces the lifetime that exists between thought and expression, the shadow between idea and reality. Even with the torment.

I can’t wait to do this again

Did you ever wake up to find

A day that broke up your mind

Destroyed your notion of circular time

When one of our kids was young, we discovered a medical condition that required years of visits to dozens of medical professionals, hundreds of tests, and many more phone calls and emails. My wife Susan took copious handwritten notes of these sessions. It was natural for her, as an English lit major and teacher, to then organize the notes into a narrative. She would sit at the dining room table at night, papers placed on the table like a tic tac toe board, entering them into a word doc. We would then show up at a new medical visit with this “essay” in hand. “Please read this, it will be easier to understand” she would say, handing the printed-out 20-page narrative to a perplexed-looking doctor.

I often wonder if they ever read this essay.

These were, well, dark times. The essay allowed us to make sense of the darkness, the information, to have something more bright and solid to hold onto in the swirl of the vague diagnoses.

The essay also got longer and longer. At one point a friend read it and said “you have a book here.”

Susan spent the better part of the next year evolving the essay into a book - a memoir of a few years’ time, a tale about the intersection and dysfunction of medicine meeting humanity. As memoir the manuscript was written in chronological order - from day 1 of our son’s life through year four.

She printed out this timeline-based memoir on a stressed-out HP inkjet printer that rattled like the subway as it printed, and walked it around Manhattan, dropping it off at agents and publishers alike. Rejection after rejection followed.

* * *

David Epstein, the author of Range, writes about how a simple change in perspective can unlock craft, quality and creativity:

When I worked as a fact-checker earlier in my career, a colleague gave me the excellent advice to go backward through any article I was checking, ticking off each fact as I went. When I only went the usual direction, I found I always just unconsciously glanced over something.

By reviewing the articles backward he noticed more things.

Tony Fadell, the founder of the Nest thermostat, similarly describes that invention as a way of looking at something familiar in a new way:

You see, when you're tackling a problem, sometimes, there are a lot of steps that lead up to that problem. And sometimes, a lot of steps after it. If you can take a step back and look broader, maybe you can change some of those boxes before the problem. Maybe you can combine them. Maybe you can remove them altogether to make that better.

What did they do? Put an algorithm in that would simply watch to understand the temperature you used - when you got up, or when you went away - and program the thermostat automatically.

* * *

I backpacked through Southeast Asia when I finished school. I found myself in a town called Surat Thai after spending a month on the islands off the eastern coast of Thailand. While these islands were a paradise of white sand beaches filled with British and Australian ex-pats, I was ready to go visit Malaysia. My friend Keith and I walked from a hostel one blistering humid morning to a shaded bus station half a mile away, looking to board a $5 bus towards a town called Hat Yai. We couldn't find a posted bus schedule anywhere in the weathered wood bus station. There were a few locals meandering around, including an older gentleman wearing a blue hat and vest, official-looking clothes we presumed. In broken language with our Lonely Planet pages open to our destination, we asked him what time the bus might be coming.

“Yes, the bus south is coming” he kept replying to our questions in his likewise broken English, listening intently each time we repeated ourselves over and over.

We were perspiring as if we were still swimming in the oceans of the beaches we just left, as we pointed to our wrists, some kind of universal signifier for “what time.” He just shook his head. “The bus will come, the bus will come.”

Two days later we finally caught the bus south simply by showing up, sitting down and just waiting for 90 minutes. The man was right - the bus did come, just on a more organic schedule than the rigid one we expected. We got to Hat Yai hours later.

With some mixture of perseverance and passion, Susan kept sending the manuscript to people even in the face of rejection. Months later, one agent responded excitedly. She offered to attempt to get the book published. She had, though, one requirement: rewrite the story in a non-chronological order. Susan was confused.

“You’ve written the story in a logical forward timeline“ agent said. “You instead need to write it about the feelings you were having. Organize it that way. Each chapter does not have to follow the previous one in time. You experienced all this in forward time. I need you to look at this in a different way - as a set of feelings and associated experiences..”

Huh.

Susan rewrote the story from the point of view of a collection of emotions. It read much, much better. It had flow, more like a novel. Agent pitched the book to publishers for a second go around. The publishers finally jumped; the book got published.

* * *

What if you looked at things backwards? Or out of order? What if you zoomed out and noticed something that was right there that you didn’t at first see.

What could you discover by doing that?

Back in college, a few friends were studying in the UK. One night they walked into a pub, saw a bar-band playing and fell in love. They made excited calls back to us in the States; they mailed cassettes of the band playing, the handwritten setlists filled with exclamation marks.

A plan was hatched.

We knew nothing about anything but were avid readers of music books and biographies, of Rolling Stone articles.

We decided we would fly the band over for a week, put them up in dorms throughout the school, introduce them to everyone, and end the week with a big house party on a Saturday night where the band would perform. Fame and fortune would result. The band readily accepted, we offered to pay them in free room and board and contraband.

A few months later the plan became reality and the band was in the US. The week was spectacular, they cruised around campus as wannabe celebrities. As newly-minted managers and promoters, we realized we needed a PA system. We took up a collection and bought one along with high-quality speakers. We hired a crew with a stage and lights to set up and break down. Saturday night - the night of the concert - expectations and nerves were high. The house was packed. We DJ'ed the first few hours before the band took the stage around 9 pm.

They launched into their first song, the sound was great, the crowd was surging.

Halfway through that song someone pulled the fire alarm in the building. Lights went on, alarms blared loud. Firefighters and police showed up. The party was over, the show was over, the evening ended.

And just like that, our illusions - delusions - were finished (and when the hangovers ended sometime the next day, we discovered someone had stolen the PA system and speakers).

* * *

In high school, we knew this kid - D - who dreamed of competing in the Golden Gloves boxing tournament. He trained all year for his opening match. We bought him a robe with his name stitched on the back. We traveled to Queens for D's first match in his march for the title. For that march, he drew an opponent - I still recall his name: Julio "El Gato" Cruz. We sat in the front row screaming our heads off. The bell rang, D and El Gato met in center ring, tapped gloves and the fight began. El Gato swung once, hitting D on the chin with an uppercut. It was as if D's body floated upwards in slow motion, feet first head second, to where his body was perpendicular with the ring for a split second. His body then came slamming down. He was out. Match over. El Gato maybe went on to win the tournament.

* * *

When the fire alarm went off and the party ended, the band was playing the REM song Driver 8. When that Golden Gloves fight ended, we drove back in this kids parents’ car - a decommissioned yellow checker cab repainted grey, fold up back seats intact

* * *

I wrote a business plan back in 1998 for a direct-to-consumer digital book service. Pre-Kindle, pre-iPad. I recently found the plan - “digital delivery of previously unavailable titles, author compensated directly.”

* * *

Is there a way to evaluate the almost-dreams that became forgotten-memories? Or is there value in them simply having occurred? Maybe they aren't lies. Instead, the "adjacent possible" reminds us that there is a "shadow future, hovering on the edges of the present, a map or guide to all the ways in which the present can reinvent itself."

In other words, maybe the expense of emotional courage in and of itself is enough.

Jean-Michel Basquiat - Untitled, 1981

Estimated value $300,000-400,000

Yet, one of the superpowers of connected technologies - networks - is that they will remove scarcity if at all possible. Connected networks by definition make things abundant that were once scarce. They broaden access. Without judgment. Removing scarcity is a way to create new types of value.

2/ What is art? One can think of art as anything - images, music, video, gifs, text, memes. Anything really.

Art also is a mirror. That is, it reflects the world back to us so we can see it more clearly. In that way, art is not simply important, it is indispensable. The Velvet Underground’s first record - The Velvet Underground and Nico - lists the artist Andy Warhol as a producer. That record’s cover art is a Warhol print of a banana. The album contains the song I’ll Be Your Mirror:

I'll be your mirror

Reflect what you are, in case you don't know

3/ Maybe digital art and non-fungible tokens (NFTs) are relevant here. A digital file, when intersected with the ubiquity and scale of the internet, can be “seen” by anyone. NFTs push the notion even further. By adding to the ideas of abundance and scale those of passionate distribution, patronage, the day-one fan and, yes, ownership. Concepts associated with scarcity, now distributed out to the abundant world at large.

Yes, there is no limit on the supply. Yet, connected networks make things that were scarce now abundant.

4/ NFTs and cryptoeconomics (tokens) in general force the ownership issue by allowing for everything to be, and governed by, a market. This is neither good nor bad - it is, though, very different. Worth considering more.

At the same time, I wish Warhol was around to see this. In many ways, he conceived of and predicted it more than 50 years ago. He was explicit that art meant business and business meant art. In an inversion (or provocation) about the notion of artistic creation, he called his studio The Factory. He also said: “You know it’s art when the check clears.” And:

Being good in business is the most fascinating kind of art.

Making money is art and working is art and good business is the best art

Another artist (Jay-Z) reflected this concept back to us in his 2005 lyric:

I’m not a businessman; I’m a business, man

Artists taking agency over their own economics is not new. Maybe what is new is - again - the scale and abundance, that more people can experiment with this notion of artistic agency.

5/ I love Warhol’s Campbell’s soup cans. I could look at them all day. Not for the brush strokes - these are silkscreen printed - but for the representation of the world they reflect. A Warhol soup can looks exactly like the actual cans. Thus, they mean something different about art by trying to tell us about commerce and ourselves. Warhol himself decried almost any notion of creativity and agency in his works, via technique:

I find it easier to use a screen. This way, I don’t have to work on my objects at all. One of my assistants or anyone else, for that matter, can reproduce the design as well as I could.

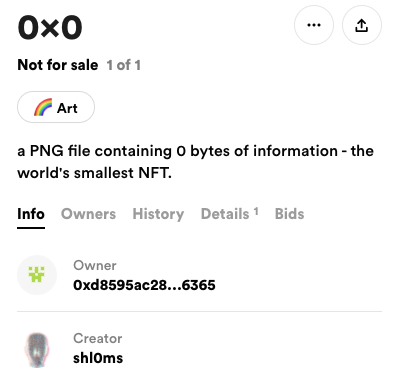

Here is a piece of art and associated NFT - “a PNG file containing 0 bytes of information - the world's smallest NFT” - by the artist shl0ms:

This reminds me of John Cage’s piece 4′33″ - a score that “instructs performers not to play their instruments during the entire duration of the piece.”

Mamet once wrote “a great meal fades in reflection. Everything else gains.” What he meant, I think, was that it’s not the thing that matters, but the thing about the thing. The context of the thing. How you experience the thing. NFTs enhance this by providing for a supercharged way to understand the text and the context (and the money context) all at the same time.

John Palmer wrote an essay minted as an NFT. He called it the “first community-owned essay, crowdfunded on Ethereum.” The writing - Scissor Labels - is wonderful: thoughtful, quirky, idiosyncratic and long; it covers design and music and cultural theory and software and hyperpop. It is a mirror.

6/ I wrote about this 5 years ago in discussing a company called Mediachain, which asked us some questions. How do you show what is behind a digital thing, understand it, pay for it? This still feels new today:

We might be able to find out the identity of the photographer, send her a micropayment, see what social network it originated on, see the press the image received, find more images by her and any number of other things.

Back then, there really weren’t tokens or NFTs. So now, when you have a digital thing, powered by an NFT, more new questions arise: shall I own it, display it, port it, trade it or sell it?

Questions that perhaps force us, again, to look into the mirror.

When I worked at AOL, we typically worked from 8am until 9 or 10pm. At the end of every day, we'd congregate in the office of our boss, to sit around and bullshit and catch up on email and talk about deals we were working on and issues in those we were facing.

One evening we were doing this, and the conversation turned to the renewal of a content distribution deal with The New York Times, one of AOL's largest and most important partners. The difficult issue here, as with most of these, was whether AOL could demand exclusivity in exchange for distribution. For example, we knew AOL members loved the Times' crossword puzzles. We wanted them for ourselves, or at least before they went up on the Times' website. The Times wanted to limit exclusivity, or at least get paid. We believed our distribution was so massive that it alone was a fair exchange for some exclusivity. Thus, the deadlock.

I remember this conversation, sitting around the conference-like table in that corner office, 4th floor of a 5-floor building. Winter was outside and the view from the windows of the Dulles, Virginia office reflected the black and cold early evening.

Bob Pittman, the President of AOL, walked around the corner and stood in the doorway. This was relatively early in his tenure at AOL, yet he was known to us already as a media and business legend.

"What's going on?" he asked, smiling. Our boss replied by explaining in detail the exclusivity issue, the various choices and options we had, questions about where we might push and where we might give.

Bob listened. He paused for a moment and replied:

"You'll figure it out. Have a good evening."

He lightly tapped the office door with his open hand twice, as if he was slapping it five. And then walked off.

There was a moment of silence before we got right back into it. We figured it out - or at least we tried. Ultimately, we didn't appreciate the move to the more "open" web would have on the proprietary AOL platform; nor would the Times appreciate the traffic AOL brought and our ability to allow them to experiment on a new generation of Internet users. We met somewhere in the middle, maybe even paid them, and it turned into a relatively good relationship over the years.

The thing is, maybe we got it right. Or maybe we didn't. I assume Bob knew that. I'd also like to believe he didn't really care. Or rather, he cared about the outcome but equally cared about making sure his team - us junior members - thought for ourselves. To empower us. To demonstrate his trust in us by specifically letting us make the decision. And figure it out.

A formative idea for a younger me: give the people who work for you a chance to resolve complex issues on their own.

Mark Randolph, the co-founder and initial CEO of Netflix, writes about this in his book, That Will Never Work. He describes what he came to understand about managing people:

What they really want is freedom and responsibility. They want to be loosely coupled but tightly aligned.

There is no way Bob, or anyone else in that room, remembers that evening. Yet I do, in detail, years later.

And still find myself saying to people "you'll figure it out."

I attended a "progressive" (read: hippie) school on the Upper West Side called Walden. In 2nd or 3rd grade, our teacher Gloria pulled out a record player every morning and let us dance around, I'm sure as a way to help burn off the energy of a large group of seven-year-olds.

She played the same song for us, every day, at the same time. The song's chorus was "Get No" and we would shout and dance around, screaming "Get No!" I remember the dance, the singing, the names of the kids, and the way it set up the rest of the day.

This class picture might have been from that year:

"Twenty minutes a day, five days a week, hosted by Michael Barbaro and powered by New York Times journalism"

Prior to The Daily, news podcasts existed. Yet, The Daily has consistently been one of the most listened to podcasts, maybe one of the most listened to of all time. Here's a chart of the New York Time stock price from January 2017 (when The Daily launched) to the present: